Source WeChat public number: National New Strategy Research

On July 19, 2017, Guosen Securities Economic Research Institute held a conference call on the sustainability of cyclical stock market and investment opportunities. This conference call, United Nations letter strategy, steel, coal, building materials, chemical industry analysts, on the current cyclical stocks Investment opportunities have been exchanged in depth. The following is the summary of the conference call:

Strategy: Reassessing the value of superior enterprises, paying attention to the fact that real estate continues to exceed expectations (Yan Xiang)

In the mid-term strategy meeting of Shenzhen in July 2017, Guosen Securities clearly put forward the view that it looks at the top 19 market conditions. Since June, Guosen Securities has held two special teleconferences on the cyclical stocks (June 13th, “National Credits, 2017, 15th: After the storm, look at the investment opportunities of the cyclical stocksâ€, July 4th Guoxin Point Gold • 2017 No. 18: Whether the cyclical stock market can continueâ€). Today, the cyclical stocks performed very well.

From a strategic point of view, today I want to talk about two main points. First, the market style is conducive to the revaluation of the dominant companies in the low-valuation period. Second, the macroeconomic data in the second quarter exceeds expectations and become the direct trigger for the start of the cyclical stocks. The possibility of continuing to exceed expectations is not ruled out.

I. Low valuation advantage Enterprise value revaluation

In 2017, the overall style of the market is to pursue the leading enterprises in the industry. We believe that there are two main logics behind this style. First, the growth rate of the industry has slowed down in the medium term, and the logic of shifting the market focus from growth to industrial concentration has not changed. Second, in the short-term, the fundamentals of the traditional industry of the motherboard have seen a significant rebound. This view has been repeatedly mentioned in previous reports.

Under the big logic of “the overall growth rate of the industry is slowing down and the strength of the dominant enterprises is strongerâ€, we believe that the style of the market chasing low valuation and high profit advantage enterprises will not change in the short term. With the changes in the short-term fundamentals of various industries, it is expected that the second and third batches of new and advantageous enterprises in different industries will once again become hot spots in the market. Looking at it now, after the “pretty 50†in the early stage of consumption, the cyclical stocks have become the second and third batch of new and advantageous enterprises in different industries. The market has moved from “beautiful 50†to “diffusionâ€.

Low valuation is a particularly important core variable if it recognizes the logic of benefiting the dominant firms in the industry concentration process. Because the purchase is the valuation of the company's medium and long-term industry status, the lower the natural valuation, the greater the flexibility. So we think that looking forward to the second half of 2017, the low valuation variable may be more important than before. The current low valuation companies of A-shares are mainly concentrated in the financial, real estate, and cycle sectors.

Subsequent industry analysts will also say that, in fact, after this round of economic cycles, the volatility of the performance of the leading enterprises in the cycle sector will be significantly reduced, which also confirms the benefits of the dominant enterprises in the process of industry concentration. logic.

Therefore, in summary, the dominant companies in the cyclical sector have a low valuation value revaluation demand in the medium term.

Second, pay attention to the possibility that real estate investment continues to exceed expectations

The direct trigger for the rapid start of this round of cyclical stock market may be that the macroeconomic data in the second quarter exceeded the expectations significantly, especially after the real estate sales and investment data continued to tighten in the first quarter of real estate policies, April-May. There was indeed a significant decline, but it rebounded sharply again in June, making the market’s previous pessimistic expectations for the real estate market significantly revised.

In the first half of 2017, the growth rate of real estate sales area is so high, it is expected that the growth rate of subsequent real estate development investment will still have an upward pulse. It is expected that the growth rate of subsequent real estate development investment will be much higher than expected, which is not the original estimate of the annual full year -2% to +2% growth rate can be stopped.

From January to June, the total amount of real estate development investment was 8.5% (compared with 7.9% in June), and the new construction area of ​​housing in January-June was 10.6% year-on-year (14.0% in June). From the current situation, the growth rate of real estate development investment for the whole year may continue to be above a very high level of 8% to 10%, and it is also possible to see a monthly growth rate of 10% in real estate development investment in the second half of the year. of. Here are two pieces of evidence to support:

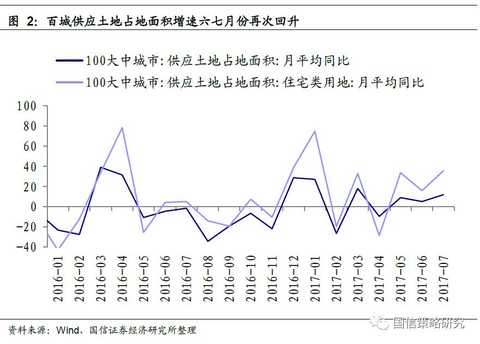

First, from the sales-to-investment lead, sales are about a lead investment of about 5 months (Figure 1). Sales rebounded sharply in June, meaning that investment may continue to rise in around November. Second, from the perspective of land transfer supply, the growth rate of land transfer supply in Baicheng in June and July increased significantly, supporting the growth of subsequent real estate investment to continue to rise (Figure 2).

Steel: Clear three main lines of policy, supply is difficult to increase, demand exceeds expectations (Wang Haitao)

First of all, we must re-emphasize this year's policy and the purpose of the policy. This year's policy is mainly three lines, the bottom line: the goal of completing the production capacity of 50 million tons; the red line: shutting down all the intermediate frequency furnaces; on-line: to prevent the sharp rise and fall of steel prices.

The purpose of the policy is to continue to make profit for steel companies and to reduce the debt ratio below 60%. At present, the debt ratio of large and medium-sized steel enterprises is 70%, and the annual profit is about 100 billion yuan. The production capacity will be reduced to 60% by 2020. In addition, China's steel industry is a typical cyclical industry, but it has its own characteristics, the loss period is relatively long, and the profit period is relatively long. The long period of loss is mainly due to the slow production capacity, because there are a large number of state-owned enterprises in it. The long profit period is due to the difficulty in obtaining new capacity indicators and bank loans, and the supply is difficult to increase. Therefore, on the whole, we are very optimistic about the profits of steel companies. However, it is not entirely optimistic about the price of steel, mainly because there is no supply side reform of iron ore and oversupply. The fall in iron ore prices will also drive down the price of steel, which is more prominent in April/May. Under normal circumstances, steel companies have a month or so of iron ore stocks, iron ore prices will cause iron and steel enterprises to produce low-priced steel with high-priced mines, profits will be adjusted back. However, the current iron ore price is also at a medium level, and the future decline is limited, so steel prices and steel companies' profits are more guaranteed.

From the demand point of view, this year's demand is still very much higher than expected, and the macro data released on the 17th once again verified this point. From January to June, fixed asset investment increased by 8.6% year-on-year, and the growth rate was unchanged from January to May. In June, the new construction area and sales area of ​​housing increased by 14% and 21% respectively, of which the new construction area increased at a new high this year, and the real estate sales area was the second highest. This indicates that steel consumption will remain at a high level in the next 3-6 months. From the first half of July, the consumption of rebar has been increasing.

From the perspective of supply, the restrictive link is still limited in steelmaking and ironmaking capacity. Last week, the weekly output of rebar was 3,343,400 tons, an increase of 17,400 tons on a week-on-week basis; the weekly output of wire rod was 1,422,000 tons, a decrease of 12,200 tons on a week-on-week basis. The output of hot coil was 3.241 million tons, an increase of 14,900 tons on a week-on-week basis. Production has risen and fallen. Due to the sufficient capacity for rolling steel, steel companies can only allocate the limited ironmaking and steelmaking capacity to the most profitable varieties, but the total production increase is also very limited.

From the perspective of inventory, social stocks have been declining, basically reaching the historical minimum. Among them, Mysteel statistics showed that there were a slight decrease in rebar in 35 major cities on the 13th, with rebar stocks of 3.875 million tons, down 22,300 tons from last week. The inventory of hot coils in 33 major cities was 2.204 million tons, a decrease of 50,800 tons from last week. Prices are more likely to skyrocket when stocks are at a lower level.

In addition, from the futures of rebar and hot coil, we can see that everyone is more optimistic about future expectations. Among them, the futures rebar discounted water dropped from the highest of 700 yuan to the current basic flat water state.

From the recommendation target, Baosteel Co., Ltd. is mainly recommended. Due to the large performance support of Baosteel Co., Ltd., Zhanjiang Project is expected to contribute a profit of RMB 2-30 billion this year. Moreover, the third blast furnace in Zhanjiang is under construction and will be more optimistic in the future. In addition, Nangang is recommended, and Nangang is located in Jiangsu Province. The local blast furnace operating rate is over 98%, the blast furnace operating rate is high, and the production capacity pressure is high. In addition, as the main products of the company are medium and heavy plates, the price of plate is rising significantly. In addition, there are 3 million tons of rebar, and the rebar has a gross profit of around 1,000 yuan. Therefore, it is estimated that the profit of Nangang will be around RMB 2.3-2.5 billion this year, and there is still a large room for the stock price to rise. In addition, the lower valuation of Maanshan Iron & Steel Co., Ltd. is also recommended.

In addition, the iron alloy standard Erdos is recommended. As the government has proposed to thoroughly investigate rebar, the rebars of some small enterprises in China have increased the strength by “wearing through water†and reduced the amount of silicon-manganese alloy added to reduce costs. However, on the one hand, the water-through rebar is easy to rust, and although the strength is required, the strength is significantly reduced in the case of an increase in the ambient temperature. Therefore, the government proposed to check the rebar composition, which will lead to an increase in the amount of silicomanganese alloy and an increase in price. Good ferroalloy production company Erdos.

Coal: optimistic about the sustainability and rising space of coal stocks, continue to push the coking coal stocks (Wang Zheng)

1. We expect this round of coal stocks to continue to rise and the space may be higher than in the past. The main reason is that this time the interim results exceeded the expected release and the correction of macroeconomic pessimistic expectations, coal stocks ushered in Davis double-click. The main factor leading to macroeconomic corrections was that property and macroeconomic data exceeded expectations in June. As long as the future macro expectations are no longer pessimistic, the valuation of coal stocks may continue to be repaired. From the historical average valuation, the coal stocks still have a lot of room to rise.

2. The mid-term report exceeded expectations and led to an increase in the full-year performance forecast. Previously, the market worried that coking coal's decline in the second quarter will decline, but the latest results announced that coking coal stocks Xishan Coal, Pingmei, Jizhong Energy, Shenhuo shares are equal to the first quarter results. In the third quarter of June, the coking coal price in the coking coal season is expected to continue to rise, and the third quarter results will continue to grow.

3. The valuation is lower than the historical average and the repair space is large. The increase in performance will also cause the valuation to be repaired. Looking back at the period of stable performance in 2010-2013, the average PE (TTM) values ​​of coking coal stocks, Pingjiang, Pan'an, and Xishan coal were 17.6, 20.9, respectively. 17.0, 24.7, as of today's closing, according to the interim report *2 or Q1*4, the four companies' PEs are 12.0, 13.7, 14.0, and 18.4, respectively. The return to the historical average is still 47%, 53%, 21%, and 34%.

4. Investment suggestion: On the early morning of 19th, we will focus on the opportunity of coking coal stocks. The recommended flat coal stocks will take the lead in daily limit. At the moment, we are still optimistic about the sustainability and rising space of coal stocks. Coking coal stocks ushered in Davis double-click and continue to push [ Pingmei Co., Ltd., [Panjiang Shares], [潞安环能], [西山煤电]. Pingmei Co., Ltd. and Panjiang Co., Ltd. have low valuations in coking coal stocks, and there is a large space for future valuation restoration. Both Lu'an Huaneng and Xishan Coal and Electricity are high-quality metallurgical coal enterprises in Shanxi, and there is a strong expectation of state-owned enterprise reform.

Building materials: performance volatility has been greatly reduced, and the value of leading enterprises has been revalued (Huang Daoli)

First, from the perspective of the cycle

For the traditional building materials cement, glass: before the expectations of the demand side is too pessimistic, the real estate data in June, the performance is good, so that the market has the enthusiasm to do more cycles, we expect the overall demand pressure is limited in the second half, It is not excluded that the growth rate of real estate investment may exceed expectations. Therefore, we believe that the price of cement and glass in the third and fourth quarters should not be excessively pessimistic. At present, the industry inventory is still at a historical low level, environmental protection is strictly controlled, and the industry self-discipline is well implemented. Cement is expected to raise prices further (currently showing a slow downturn in the off-season), glass prices remain high, and the number of production lines that have reached the cold repair conditions this year is large. Currently, the capacity of the country is about 900 million heavy boxes, and this year it will reach the cold repair conditions. There are 185 million heavy boxes. It is not excluded that the supply contraction may exceed expectations in the fourth quarter of this year and the first quarter of next year.

Second, from the perspective of value investment and quality enterprises

The period of high-speed expansion of industry supply and rapid growth of demand has passed, and the gap between supply and demand has gradually converges. At the same time, policies such as strict control of production capacity and strict control of environmental protection have continued, and factors such as strengthening self-discipline in the industry have become the adjustment of supply and demand in short-term industries or local areas. The key elements are expected to converge at this stage, and it is expected to enter a relative steady state. If this is the first point, the performance fluctuations of the leading companies in the cyclical stocks will not be as large as before. Secondly, the operational efficiency of enterprises and cost control We will become the key to competition; we believe that high-quality enterprises rely on scale advantages, cost advantages and product advantages. In this period, management efficiency and operational efficiency will gradually be reflected, and relative competitive advantages will be highlighted; for example, our flagship group, last year The performance of 8.4 billion, of which the cost control and efficiency improvement contribution of more than 90 million, this is the embodiment of competitiveness, this year is expected to further improve this, is expected to reach about 100 million.

In addition, due to the end of the industry's rapid expansion of production capacity, the company's expenditures have begun to decline sharply. At this time, the advantages of operating cash flow of leading companies are reflected. For example, last year, Conch's performance of about 85 billion yuan, operating Net cash flow exceeds 13 billion, Qibin has 840 million performance, and operating net cash flow exceeds 1.6 billion. With such a good cash flow, we have also observed that Conch's dividend ratio has increased year by year in recent years. For example, this year we expect the dividend yield to exceed 3 points. Such a dividend rate level actually increases the safety margin of the company's stock price, and then considers that the future performance volatility is greatly reduced, the entire leading quality enterprises are facing a revaluation, and the valuation is improved.

Third, talk about the northwest

Last week, we issued a comprehensive review of the Northwest Cement Market, "Spring Breeze Second Degree Yumen Pass", which we mentioned: Northwest cement sales have rebounded from December to December, and have turned from negative to 1.04%. Up to 5.6 percentage points. Regional prices have performed well this year and stocks are at historically low levels;

Regional demand also performed better: 1) Real estate investment support slightly exceeded expectations. The growth rate of regional real estate investment in the first five months was 13.2%, higher than 8.8% in the country, including 22% in Shaanxi and 16.9% in Gansu; 2) 17 In the five northwestern provinces, the total fixed assets investment target is about 5.6 trillion, with a growth rate of 18.5%. Xinjiang's data is 19.8% in January-May, and Shaanxi's 14.4% is outstanding. 3) Benefiting “One Belt and One Road†and Western Development, June this year 35 key transportation construction projects in Gansu will be started in concentration; Xinjiang will invest more than 200 billion yuan this year to improve the traffic of Tianshan North-South Highway. It is expected that many infrastructure projects will be launched, which will effectively support demand.

The recent increase in expectations of the Qilianshan Media Group reflects the expected performance of regional cement demand and supply optimization, and is expected to rekindle the market's enthusiasm for regional cement stocks. At present, the valuation of PB such as Qilian Mountain is at a lower level in the industry and has a certain margin of safety, so it is recommended to buy.

Fourth, other high quality sub-sector building materials

Most of the sub-sectors of consumer building materials show the industry pattern of “big industry, small companyâ€. In recent years, with the upgrading of consumption, the pursuit of products and service quality by consumers, the market share of each sub-industry is gradually becoming brand, channel, High-quality enterprises such as quality services are concentrated, high-quality enterprises are accumulating, and the market share is likely to increase. It is expected to be strong. There are oriental Yuhong and Weixing new materials that are very familiar to everyone. They are among the best in the industry, and we continue to recommend them. There is also a glass fiber faucet China boulder. When it comes to glass fiber, we have discussed many Chinese material manufacturers that are talking about import substitution. While glass fiber is a material, China boulder has already gone abroad and competed with Europe and the United States to grab the global market. The share of the company is regarded as the pride of China's manufacturing industry. At present, the global market share is 21%, and the R&D is very strong. The proportion of high-end products in the future will further increase. At present, we expect the company's dynamic PE to be 15-16 times this year. Have long-term investment value. Another sub-industry is gypsum board, which represents the company's Beixin building materials. The market share is over 50%, the performance is very stable, and the valuation is very low.

So in conclusion, the key targets we recommend are as follows: Conch Cement, Huaxin Cement, Qibin Group, Qilian Mountain, China Boulder, Oriental Yuhong, Weixing New Material, Beixin Building Materials

Chemical industry: supply and demand growth rate mismatch stage, industry pattern is expected to continue to improve (Gong Cheng)

Our view: The price performance of chemical cycle products in the second half of last year was only a rehearsal, and the actual supply situation of the industry was tested. In the case that the effective supply of the industry could not match the expected demand in a short time, the price of last year will be repeated again. Even repeated evolutions.

The chemical industry is still in the stage of mismatch between supply and demand growth, and the supply and demand pattern is expected to continue to improve. The supply growth rate is slow, and the existing backward and inefficient production capacity in the industry gradually withdraws from the market. The supply and demand pattern of most sub-sectors has improved. In the second half of last year, under the market demand, the overall operating rate of most sub-sectors There have been no significant changes, resulting in the price of most chemicals since the second half of last year has gone out of a relatively strong rising market. This shows that in the chemical industry's multi-year bottom operation stage, the supply and demand of many sub-sectors are balanced. In the case of sudden increase in demand, the market cannot increase effective supply in the short term. From the year-on-year change in the completion of fixed assets investment in the chemical industry, we can also see that the industry supply contraction is very obvious when the growth rate continues to decline for many years and negative growth last year. At present, the industry as a whole is still at the bottom of the production cycle.

From the demand side, in addition to the obvious decline in the overall growth rate of the automotive industry, the growth of major downstream real estate, home appliances and textiles (clothes) in other chemical industries has been very stable this year. Even the growth rate of the home appliance and real estate industries exceeds the general expectations of the market last year. Therefore, in the stage of supply contraction, the demand side is improving, the stimulation of the cyclical products in the industry will be amplified, the price of the cyclical products is expected to rise more than expected, and the long-term prosperity will be maintained.

The demand for many chemicals can be traced back to real estate-related areas. For example, products related to the real estate industry are PVC (downstream products are pipes, doors and windows), soda ash (downstream products are glass), polyurethane (including MDI, TDI, downstream demand is house insulation materials, soft furniture), titanium dioxide ( Downstream demand is paint coating), silicone (decoration materials, sealants, etc.). In the case that the national real estate market exceeded market expectations in June this year, although the prices of related products did not go out of a strong upward trend, the stock prices of these chemical-related companies have been reflected since the beginning of July.

Based on the market expectation that the growth rate of real estate exceeds expectations, we mainly recommend the PVC, soda ash and polyurethane sub-sectors that are most closely related to the real estate market. Considering the market share of the industry's dominant enterprises, the profit level is also relatively larger than the industry average. We mainly recommend Zhongtai Chemical (002092, chlor-alkali faucet, benefiting from PVC and caustic soda market), Yuanxing Energy (000683, trona faucet, benefiting from soda ash market), Sanyou Chemical (600409, viscose and soda bismuth), benefiting from Chemical fiber, soda ash market), Wanhua Chemical (600309, MDI and polyurethane industry chain leader), Zhangzhou Dahua (600230, TDI leader, benefiting from supply contraction, TDI market is expected to continue until 2018).

Sina statement: This news is reproduced from the Sina cooperation media, Sina.com posted this article for the purpose of transmitting more information, does not mean agree with its views or confirm its description. Article content is for reference only and does not constitute investment advice. Investors operate on this basis at their own risk.

Enter [Sina Finance and Economics Unit] Discussion

Enamel pin badge widely used for the following industry as a great customized, fashion & high quality accessory. And Garment industry,Such as Overcoat, jacket, suit, leisure suit, t-shirt, shirt, skirt, work-clothes, sports wear, jeans wear, trousers, pants, foot wear and so on. Bag industry,Handbag, dust bag, school bag, purse, backpack, luggage and so on. It is can be finished with logo embossed, engraved, printed, laser, Available with various different metal colors,Plated color: options of gold, silver, bronze, nickel, chrome, antique plating etc..... Material:options of brass, iron, zinc alloy, ect......

process: Stamping, Die-cast, Anti-gold, Pearlized, gold, Nickel, Anti-nickel, Pearlized, Silver, Anti-silver.Material is friendly, Non-toxic and safe, Quality control 100% inspection before packing. Spot inspection before shipment.

Enamel Pin Badge,Lapel Pin Badge,Custom Enamel Badges,Soft Enamel Pin Badge

Shenzhen MingFengXing Art & Craft Products CO., LTD. , https://www.enamelkeychain.com