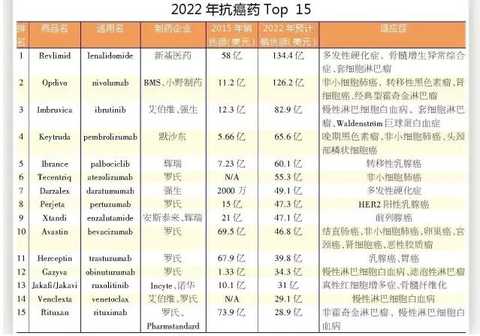

[HC360] Recently, FiercePharma released 15 best-selling anticancer drugs in 2022. It is estimated that by 2022, 15 best-selling anticancer drugs will generate nearly $90 billion in sales, accounting for Quintiles IMS. A quarter of the total US pharmaceutical market in 2014.

In this list, three PD-1/PD-L1 inhibitors belonging to tumor immunology (IO) therapy ranked in the top six. However, there is some controversy about the pricing of these drugs. Today, global drug pricing is strictly controlled by regulators and payers to a certain extent.

The huge difference between the new best-selling anticancer drug prediction list and the version three years ago shows the rapid development of the anticancer drug industry. For example, Takeda's melanoma drug, Velcade, and Johnson & Johnson's oral anti-prostate cancer drug, Zytiga, have disappeared in the list of best-selling anticancer drugs in 2022. Both will face the threat of innovative drugs and generic drugs.

Although tumor immunotherapy is accelerating, nine of the 15 best-selling anticancer drugs in 2022 are monoclonal antibodies, three of which are from Roche. These drugs are also the first monoclonal antibody drugs that will face the challenge of biosimilar drugs in the next few years, but their brand strength still helps them maintain an important market position.

1, Revlimid

For the past 10 years since the market was launched, Revlimid has been an important sales force for Celgene, the most important product in the treatment of new blood medicine, the company's expected year of 2020. Sales will exceed $15 billion, and sales of lenalidomide by 2022 are expected to double.

Xinji Medicine has spent $1 billion to expand lenalidomide maintenance therapy for non-Hodgkin's lymphoma (NHL) subtypes and diffuse large B-cell lymphoma indications, but phase III clinical failure, after which the drug continues Treatment trial for follicular lymphoma. Xinji Medicine is still confident in the importance of lenalidomide, and believes that it will remain an important sales driver in 2020 and beyond.

2, Opdivo

Opdivo, approved in Japan in 2014, was the first PD-1 inhibitor to be effective against lung cancer. Keytruda, a PD-1 inhibitor developed by Merck, was marketed in the US three months earlier.

In 2022, Opdivo will gain a leading position in a new generation of oncology drugs, but its sales are expected to be reduced by the failure of the CheckMate-026 treatment trial for first-line non-small cell lung cancer. This has made its market expansion still subject to Keytruda and Roche's Tecentriq. According to analysis, if the trial is not frustrated, Opdivo can even generate $14.6 billion in sales in 2022.

3, Imbruvica

The Bruton's tyrosine kinase inhibitor, Imbruvica, quickly broke through the start of heavyweight sales after its launch in early 2013, and is now a leader in the second-line treatment market for chronic lymphocytic leukemia (CLL).

In March last year, Imbruvica received FDA approval for first-line treatment of CLL, providing an opportunity for early recovery for more patients who still need long-term treatment. Coupled with potential new indications such as solid-state solid tumors such as non-Hodgkin's lymphoma, pancreatic cancer and acute leukemia, Imbruvica's 2022 sales are expected to be highly probable. However, in the next few years, the drug may face some fierce competition. For example, Revlimid of Xinji Medicine has shown strong ambitions in the field of lymphoma indication treatment.

4, Keytruda

Keytruda, which was approved by the FDA in September 2014, was the first PD-1/PD-L1 inhibitor approved in the United States, but today sales have lagged behind Opdivo, both in the second line of melanoma and non-small cell lung cancer. There is a direct competitive relationship between treatment and treatment of head and neck cancer. As Keytruda's first-line treatment indication for non-small cell lung cancer was approved by the FDA, and Opdivo failed to reach the primary endpoint of the indication treatment in the trial, it also gained an advantage in this competition.

At the moment, the main reason why Keytruda is less than Opdivo in second-line treatment of non-small cell lung cancer is that it must rely on PD-L1 testing, which is suitable for all patients.

5, Ibrance

Ibrance is the first drug listed in the CDK4/6 inhibitor. In February 2015, it entered the historical arena by combining letrozole with a combination therapy for hormone receptor-positive (HR+) human epidermal growth factor-negative (HER2-) and diffuse breast cancer.

This drug did not show any sales decline in 2016, and it has achieved a very impressive sales of US$950 million in the first half of the year. The increase in sales has also benefited from the second indication approval, a new combination therapy with AstraZeneca's Faslodex (fulvestrant) for the treatment of patients with worsening conditions after hormone therapy.

However, brance's potential competitors will soon follow its pace, such as Novartis' ribociclib will be approved through the FDA's priority review path.

6, Tecentriq

Roche's Tecentriq ranks third in the PD-1/PD-L1 inhibitor market, about one year ahead of Keytruda and Opdivo night markets, but soon has a place in the US bladder cancer treatment market, only in a few weeks. Within $19 million in sales, he was approved for lung cancer indications. Tecentriq's bladder cancer indications were first approved, and they are also complementing new indications such as colorectal cancer while expanding the market share of lung cancer treatment.

As a global leader in anticancer biopharmaceuticals, Tecentriq will continue to maintain considerable growth momentum based on its long-standing reputation and market position. However, Roche also needs to speed up the pace of trials and approvals for more indications, as many of the company's heavyweight drugs have begun to face competition for biosimilar drugs.

7, Darzalex

With the burden of expanding Johnson & Johnson's market share, Darzalex, a multiple sclerosis drug, was officially launched in 2015. The drug is used in four-line therapy. After the treatment sequence, which is located in Pomalyst (pomalidomide) of Xinji Medicine and Kyprolis (carfilzomib) of Amgen, Johnson & Johnson is currently trying to advance the treatment order of the drug.

In 2016, the clinical clinical data of Darzalex published by the American Society of Clinical Oncology showed that the combination of this drug and Takeda Pharmaceutical's Wanxi as a second-line treatment can effectively reduce tumor deterioration or mortality by 61%.

8, Perjeta

Perjeta, which went on sale in 2012, became the fastest growing new drug for Roche due to the approval of early HER2-positive breast cancer indications and its expansion into early treatment of other tumors. In 2022, Perjeta's sales forecast was $4.73 billion, surpassing Herceptin, a Roche heavy breast cancer drug that lost $2.8 billion in sales due to competition for biosimilar drugs.

In 2013, Perjeta received FDA approval to become the first breast cancer treatment to be used before surgery, significantly expanding the range of available patients. The drug is often combined with Herceptin or docetaxel chemotherapy to reduce breast tumor volume, the first FDA-approved anticancer drug that targets tumor shrinkage rather than increased survival.

9, Xtandi

In 2016, Pfizer's $14 billion acquisition of Medivation received great attention. Through this transaction, Pfizer got the fast-growing prostate cancer drug Xtandi.

Although last year, Zytiga, a strong prostate cancer drug with a strong momentum, was slightly better than enzalutamide with more than $2.2 billion in sales, but some of its advantages are helping to gradually shorten its distance. Enzalutamide can be used alone, and abiraterone must be combined with steroidprednisone to balance side effects. According to FDA requirements, patients receiving abiraterone need to pay attention to the level of liver enzymes in the body and be alert to the risk of toxicity.

However, enzalutamide is facing pricing pressures in the United States. CVS has removed the drug from the 2017 drug list for cost reasons, and it may also face competition from prostate cancer drugs such as Bayer's potentially powerful Xifigo and Valeant's Provenge.

10, Avastin

Avastin, a vascular endothelial growth factor (VEGF)-targeted antibody, is currently the second-largest sales force in Roche's heavyweight drug, which was first approved for colorectal cancer treatment in 2004. New indications have been added and recently approved in Europe with Tarceva for EGFR-positive non-small cell lung cancer. In 2017, its joint therapy trial with Tecentriq will be launched and it is likely to be approved for indications for mesothelioma in the future.

In 2015, Avastin’s sales increased by 9%, but it has begun to be affected by the competition for biosimilars listed on emerging markets. In addition, Amgen and Allergan also announced plans to submit their biosimilar drug listing applications worldwide last year; Biocon and Mylan in India have a biosimilar drug in review in Europe. .

11, Herceptin

In 1998, Roche's Herceptin was launched, revolutionizing the hopes of survival for HER2-positive breast cancer patients with previously bleak treatment prospects. Today, Herceptin still accounts for 90% of the disease treatment market, but since its European patents have expired in 2014, US patents have only remained until 2019, and they are now beginning to face challenges from biosimilars.

Mayan and Biocon have launched a biosimilar drug version of Canmab in Herceptin in India. Analysts believe the drug will be available in Europe in 2017 and in the US in 2018; Celltrion's biosimilar Herzuma is already available in South Korea. However, Roche's chief operating officer, Daniel O'Day, said in a conference call in the second quarter of 2016 that Herceptin will continue to grow in the biosimilar market.

12. Gazyva

Faced with the biosimilar drug challenge faced by Rituxan, a heavy blood tumor drug in 2017, Roche's hematologic oncology sector will rely more on Gazyya for B-cell malignancies, an upgraded version of rituximab. Gazyya was approved in 2013 for the treatment of early-stage treatment of chronic lymphocytic leukemia (CLL). Initially, the drug sales growth was weak, but there was a significant improvement after the approval of follicular lymphoma indications.

The results of clinical phase III trials published at the annual meeting of the American Society of Hematology last year showed that Gazyva combined with chemotherapy is more effective than rituximab in the treatment of follicular lymphoma. In addition, Gazyva has made some progress in the treatment of acute lymphoblastic leukemia in combination with acute myelogenous leukemia, multiple sclerosis and mesothelioma, and Venclexta developed in collaboration with Roche and Aberdeen.

13, Jakafi

In fact, Jakafi's ability to enter the top 15 list is slightly unexpected. Last year, Incyte announced the termination of solid-state tumor therapeutic drug development after the drug failed prostate and colorectal cancer indication tests. Jakafi was first approved for the treatment of myelofibrosis in 2011, and the 2014 indication for polycythemia has been approved, making it a solid market position in the field of rare hematologic cancer treatment.

In November 2016, the potential stage of the potential competitor, Gilead's momelonitib multiple sclerosis indication, was not smooth, which means that the market space of Incyte is still considerable.

14, Venclexta

Venclexta, a collaboration between AbbVie and Roche, is the world's first BCL-2 inhibitor, which was launched in the United States in 2016 to treat chronic lymphocytic leukemia caused by genetic mutations. The drug is currently priced at $110,000 a year and may be used in combination with Roche's rituximab for the treatment of chronic lymphocytic leukemia.

Venclexta's future competitors include lenalidomide from Shinki, Aibowei's own Imbruvica, and Gilead's new Zydelig (idelalisib). Aberdeen CEO Richard Gonzalez recently revealed that Venclexta is likely to help promote the sale of Imbrvica, or the latter has a positive effect on the former, and the combination may become the most effective combination therapy for chronic lymphocytic leukemia.

15. Rituxan

Rituxan has been on the market for 20 years and is currently the third largest sales force in Roche. So far, the drug has maintained a certain growth rate, with an increase of 6% in the first half of 2016.

However, at the end of 2017, rituximab will usher in a biopharmaceutical challenge, with sales losing $4.5 billion by 2022. Celltrion led the development of the drug-like drug. In October 2015, it submitted a listing application for the medicinal drug CT-P10 to the European Medicines Agency (EMA); the research and development of Novartis's generic drug unit Sandoz The biosimilar version submitted a listing application to the European Union in May 2016; in December 2016, Sanofi and JHL Biotech entered into a partnership with the former to spend $236 million to promote JHL's rituximab-like drugs. Stand out from the commercialization strategy.

Editor in charge: Yan Wenqian

Ladies' Tops,Ladies' Blouses,Ladies' Dresses,Ladies' Jumpsuits

Shaoxing Yidie Garment Co.,Ltd , https://www.yidiegarment.com